Understanding the terminology is a very crucial part before you make a decision to spend your money on an insurance policy. IDV in Insurance is one of the critical terms which needs to be understood correctly.

Basically, IDV is used in motor insurance such as bike insurance, car insurance etc. It stands for “Insured Declared Value” and it refers to the maximum amount that an insurance company will pay out in the event of a total loss or theft of an insured vehicle.

Why IDV is important?

IDV is an important factor for both; the insurer and the vehicle owner. The vehicle owner should ensure that IDV is not being calculated lower because it means he will get a lower claim in the event of theft or total loss of the vehicle.

Lower IDV means lower claim and higher IDV means higher claim amount. Apart from that, there are many other factors that make IDV an important factor in motor insurance. Some of them are:

- The Basis for Premium Calculation: The IDV is the basis for the calculation of the premium amount for the motor insurance policy. The higher the IDV, the higher the premium. Hence, IDv plays a crucial role in determining the cost of your policy.

- The Basis for Claim Settlement: The IDV is the maximum amount that will be paid by the insurer in case of theft or total loss of the vehicle. Thus, it is the basis for determining the claim settlement amount.

- Protection Against Under-insurance: Setting the right IDV for your vehicle is important to avoid being underinsured. If the IDV is set too low, it may not provide adequate coverage. In such cases, the policyholder may have to bear a significant portion of the loss.

- Protection Against Over-insurance: If the IDV is too high, it will result in a higher premium amount which can burden you with extra expenses. So, one should always thrive for setting the right IDV.

Now you must have understood the fact that Lower IDV means lower premium and hence lower payout while higher IDV means higher premium and hence higher claim amount in the event of loss or theft of the vehicle.

How is IDV calculated?

In general, the Insured Declared Value (IDV) of the vehicle is calculated based on its current market value and depreciation. The IDV of a vehicle is calculated as follows:

IDV = Manufacturer’s Listed Selling Price(Ex-Showroom price) – Depreciation Value

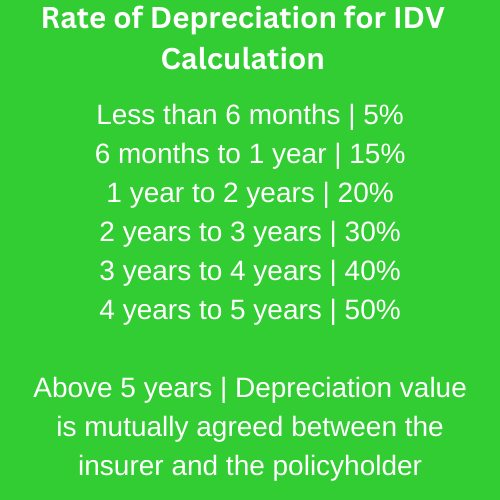

Rate of Depreciation Based On the Age of the Vehicle

| Age of the car: | Depreciation in % |

| 6 months and below | 5% |

| 6 months to 1 year | 15% |

| 1 year to 2 years | 20% |

| 2 years to 3 years | 30% |

| 3 years to 4 years | 40% |

| 4 years to 5 years | 50% |

Above 5 years, the depreciation value is mutually agreed upon between the insurer and the policyholder. Apart from depreciation, the process involves many other factors and considerations as follows:

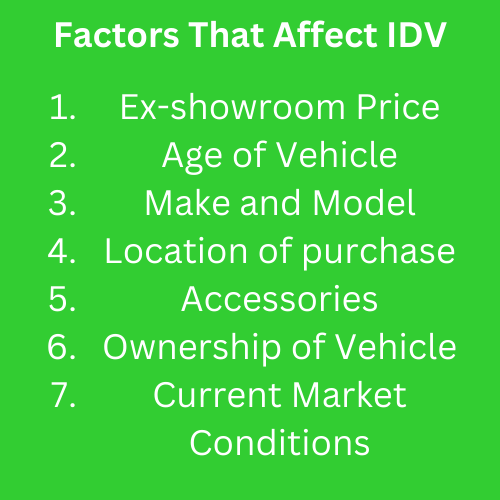

- Manufacturer’s Listed Selling Price(MLSP): This is the first thing that is considered at the time of calculation of the IDV of a vehicle. It refers to the ex-showroom price of the vehicle as suggested by the manufacturer.

- Age of The Vehicle: The age of the vehicle is a crucial factor in calculating its IDV. This is because the market value of a vehicle decreases year on year. So, the older the vehicle, the lower the IDV.

- Vehicle Make and Model: Generally, higher-end models have a higher IDV as their market value is higher. Hence, plays a critical role in the calculation of the IDV of a vehicle.

- Type of vehicle: There are many types of vehicles available in the market. Each type of vehicle possesses a different market value. For example, SUVs tend to have a higher value than sedans.

- Geographic Location: The geographic location can affect the IDV of a vehicle due to differences in market value across regions.

- Ownership of the vehicle: It is taken into consideration if the car is owned by an individual or by a company, at the time of calculation of IDV.

- Accessories: If you have added any accessories to your vehicle(car), It will affect your Insured Declared Value.

- The Current Market Conditions: The IDV may also be influenced by current market conditions, such as demand and supply.

When Is IDV Payable?

Setting the right IDV at the time of buying or renewing the insurance policy is important for hassle-free claim settlement. In case your IDV is required for the calculation of the claim amount, you will receive fair & satisfactory compensation. There are conditions when your IDV is payable:

Theft of the Vehicle: Theft of the vehicle is the most common event when IDV is payable. It is considered the total loss of the vehicle and hence the insurer has to pay the full IDV amount.

Total Loss of The Vehicle: The total loss of the vehicle caused by an accident when the repair cost exceeds the Insured Declared Value. In this condition, the IDV is payable.

Faq’s

What is the full form of IDV in Motor Insurance?

The full form of IDV is Insured Declared Value. It is calculated based on the current market value of the vehicle.

Can I Calculate the IDV myself?

Yes, anyone can calculate IDV using an Online IDV calculator. But it may or may not match the ones calculated by the insurance company.

What if I Choose a Higher IDV?

If you choose a higher IDV, you have to pay a higher premium and hence you can get a higher claim amount in the event of loss or theft.

What if I choose A Lower IDV?

If you choose a lower IDV, you have to pay a lower premium and hence you can get a lower claim amount in the event of loss or theft.